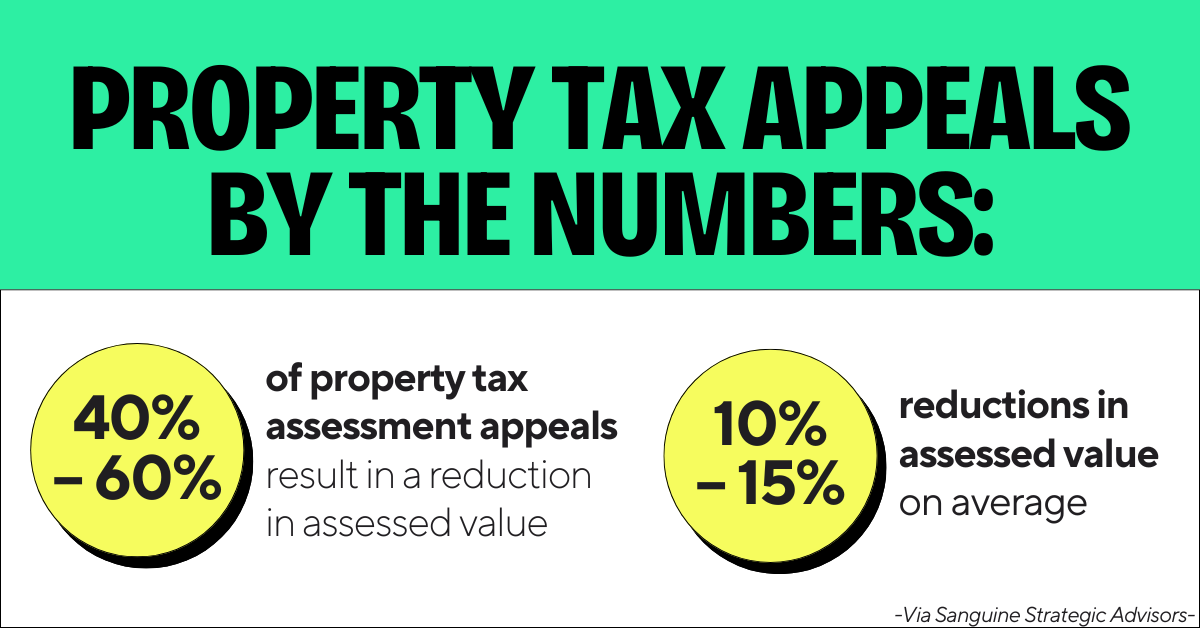

Every year around assessment season, I have the same conversation. Someone opens their mail, sees a big jump in their assessed value, and thinks, “There’s no way my house is worth that much.” Sometimes they’re right. Often, they’re not.

In Rochester and Monroe County, many homes were under-assessed for years while the market moved quickly. Prices rose, inventory tightened, and construction costs climbed. When assessments finally catch up, it can feel sudden or unfair, even when it’s a delayed correction. That doesn’t mean every assessment is accurate, but it does mean this isn’t a fight everything situation. The real question is whether challenging your assessment actually makes financial sense for you.

What Your Assessment Really Means

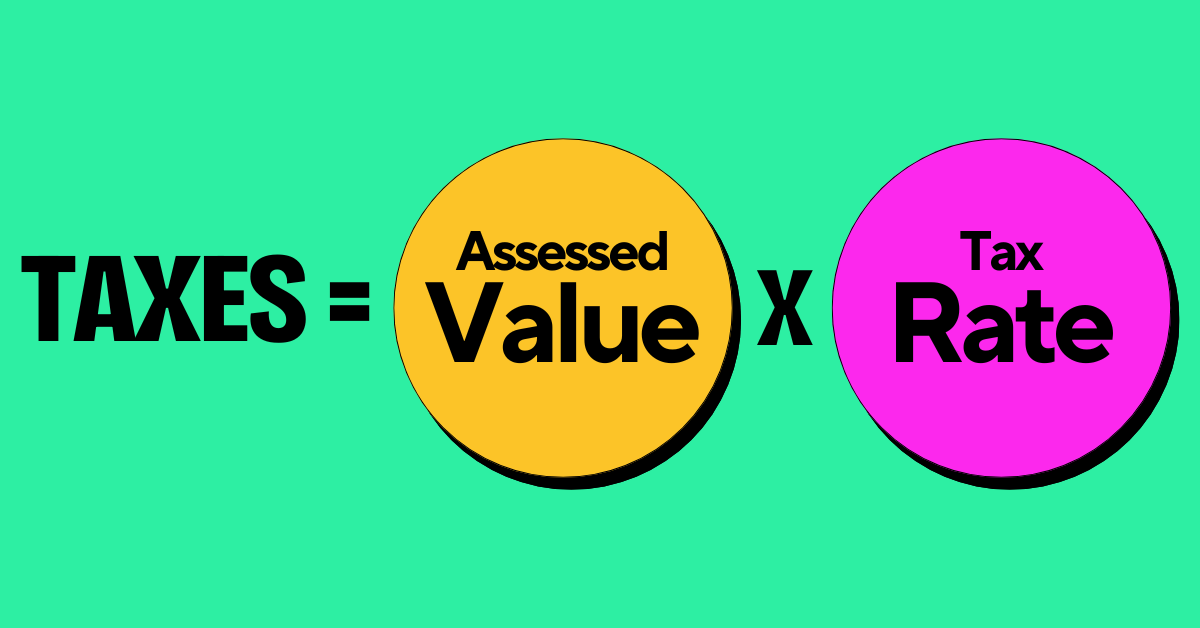

One of the biggest sources of confusion is mixing together four different things:

-

What your home would sell for

-

What the town says it’s worth for tax purposes

-

The tax rate

-

Your final tax bill

When you challenge an assessment, you are only disputing the assessed value, not the tax rate or how tax dollars are spent.

The formula is simple:

You don’t control the tax rate. The only variable you can challenge is the assessed value. If your assessment is accurate but your taxes feel high, that’s a policy issue, not a valuation one.

Why Assessments Are Rising Around Rochester

In many parts of Monroe County, reassessments didn’t happen frequently while the housing market changed rapidly. Homes that struggled to sell at $150,000 a decade ago were suddenly trading in the low-to-mid $200s. Inventory stayed tight. Buyers competed harder. Costs climbed.

When assessments finally adjust, the increase can feel shocking, but often it’s simply the math catching up. That’s why blanket advice like “always grieve your assessment” doesn’t hold up. Sometimes the increase is justified. Sometimes it overshoots. The only way to know is by looking at real data.

When Challenging Your Assessment Makes Sense

There are situations where filing a grievance is worth the effort:

-

The assessed value is meaningfully higher than recent comparable sales in your neighborhood

-

The town’s property data is factually wrong (square footage, bathrooms, condition)

-

Your home has real condition limitations that buyers would price in but models may miss

-

Nearby similar homes are assessed inconsistently

As a general guideline, if your assessment is within a few percentage points of market value, the effort often isn’t worth it. Once the gap approaches 10% or more, it becomes worth examining more closely.

Evidence matters. Frustration doesn’t.

When It Probably Doesn’t

Challenging your assessment usually doesn’t make sense if:

-

You bought recently and the purchase price supports the assessment

-

Comparable sales clearly justify the value

-

The potential savings are minimal

-

Your argument is based on what the home used to be worth, not current market data

Hope is not a valuation strategy. Sometimes the right answer is doing nothing.

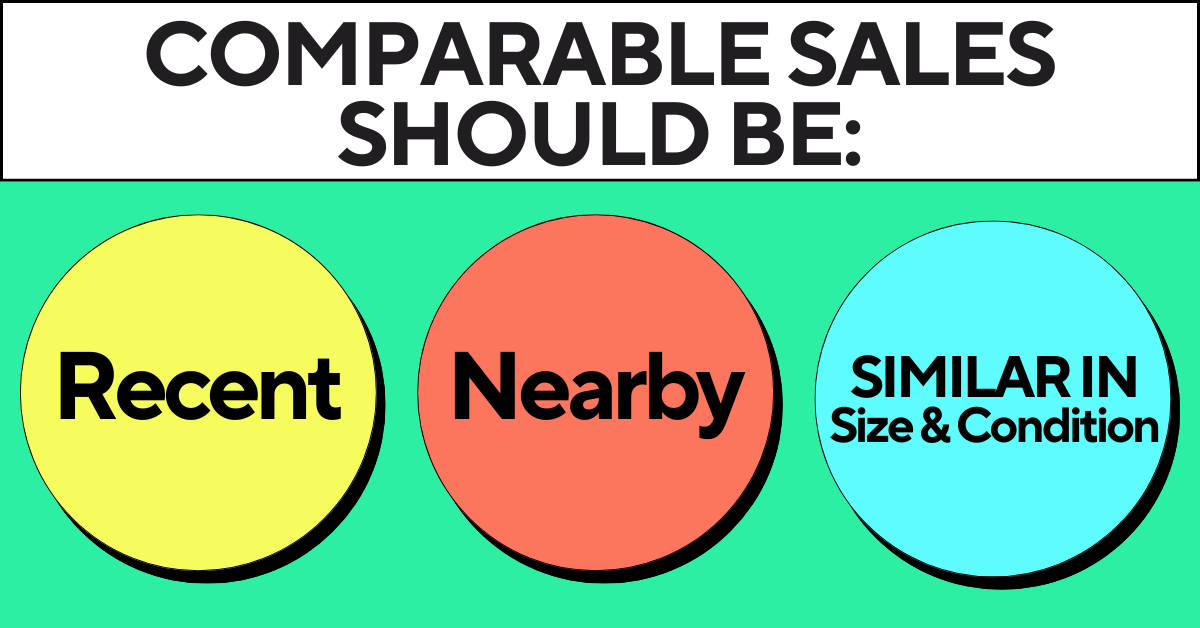

How to Sanity-Check Your Home’s Value

You don’t need to be an appraiser, but you do need the right lens.

Look at recent comparable sales that are:

-

In the same neighborhood or school district

-

Similar in size, style, and layout

-

Sold under normal conditions

-

Not distressed or unusual transactions

The goal isn’t to cherry-pick the lowest sale. It’s to understand what buyers are actually paying for homes like yours today. Online estimates can help directionally, but they’re not a substitute for real comparables and local context.

What the Grievance Process Looks Like

At a high level:

-

Some municipalities allow informal reviews before formal filings

-

Formal grievances are reviewed by a Board of Assessment Review

-

Deadlines vary by municipality, so timing matters

-

Additional appeal options may exist in certain cases

The process isn’t overly complex, but it does require organization and documentation.

Is the Juice Worth the Squeeze?

Before moving forward, run the math:

-

How much could this realistically save per year?

-

How long will you own the home?

-

How strong is the supporting data?

-

What’s the likelihood of success?

A $20,000–$30,000 reduction in assessed value can matter over time. A $5,000 reduction often doesn’t justify the effort. This is a financial decision, not a moral crusade.

The Big Takeaway

Your home is likely your largest financial asset. Decisions around it deserve more than knee-jerk reactions and internet noise.

If your assessment jumped, don’t assume it’s wrong, but don’t blindly accept it either. Look at the data. Understand the market. Run the numbers. Make a clear-headed decision.

And if you want a second set of eyes on your situation or help understanding what’s happening in your part of Rochester, you can start that conversation here:

👉 https://www.anthonybuterateam.com/contact/